The MR Tanker Reckoning: A Supply Crunch is Coming

In a very recent feature in TradeWinds, citing our brokerage insights, one conclusion stands out: the MR tanker market is approaching a structural inflection point.

A significant portion of today’s fleet was ordered and delivered in the second half of the 2000s. As these vessels approach and exceed 20 years of age, replacement pressure is set to intensify. At the same time, MRs continue to play a central role in today’s refined product trade, increasingly so, and in some cases at the expense of Handysize tonnage.

This dynamic is unfolding in a market already showing strong momentum. Several shipyards report MR orderbooks effectively committed through 2029-2030, with important cross-sector competition for yard capacity further constraining access to slots.

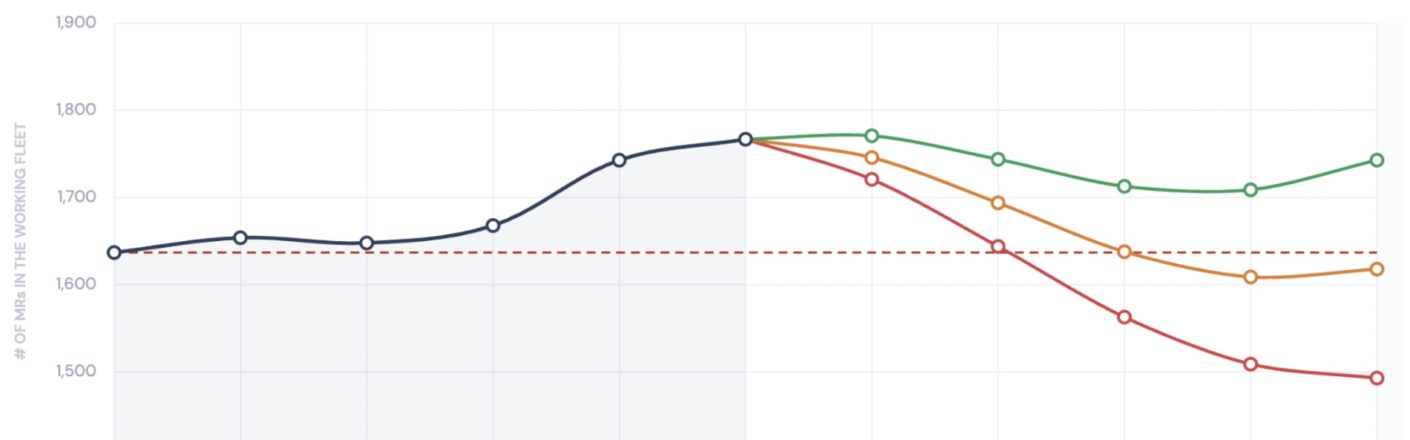

The attached graph highlights a critical inflection point:

• The current total working MR fleet peaks around 2027

• From 2028 onward, supply dynamics become highly sensitive to newbuilding intake, as a significant cohort exits the working fleet

• At 50 newbuilds per year, the fleet contracts materially by 2032

• Even at 75 newbuilds per year, supply drifts below 2022 levels

• Only at ~100 newbuilds per year does the fleet stabilize around 2026 levels

A key leading indicator will be the market’s absorption of the 2026-2027 MR delivery wave. If freight rates remain resilient despite the near-term influx, it would point to strong underlying demand, potentially setting the stage for structural supply tightening in the outer years.

Ultimately, the trajectory of freight rates will hinge on delivery timing and scale, the resilience of underlying demand, and the evolution of tonne-mile dynamics.

👉 Read the full article in TradeWinds : https://lnkd.in/ejsPC3Fs

Want deeper insights into today’s market dynamics? Contact us to discuss.